Daily Market Commentary

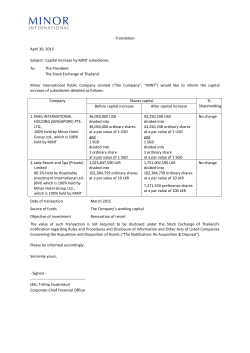

ABC 28 January 2015 Sri Lanka Sri Lanka Markets Update Daily Market Note Domestic Markets HSBC research is available online: USD/LKR spot closed at 133.15/40 against an opening level of 133.10/35. Spot opened trading today at 133.15/40 and is currently trading at 133.20/45. Overnight liquidity was a surplus of LKR 11.8 Bio and O/N Money averaged at 5.82% Source : Reuters (24/11/14) Internet http://www.hsbcnet.com http://www.hsbc.lk Reuters HSBS Disclaimer This report must be read with the disclaimer, disclosures and analyst certifications on p4 that form part of it. Issued by The Hongkong and Shanghai Banking Corporation Limited. Source : Reuters (24/11/14) Regional Currency Performance against USD LKR -0.27% THB -0.24% Contacts -0.05% BDT INR 0.39% IDR 0% 0% 0% 0% 0% 0% Local currency depreciation/appreciation 0.21% 0% 0% 0% Source : Reuters (01/01/14 to 24/11/14) CBSL left policy rates unchanged with standing deposit rate at 6.50% and standing lending rate at 8.00%. Access to standing deposit facility remains rationalized at 3 times per calendar month, deposits exceeding 3 times will be accepted at 5.00% PUBLIC Head of Sales Perry Savundranayagam 1% 2421697, 2334222, 2325435 Corporate Sales Eraj Rajapakse DO Arundhaka Dep Rajiv Jayawardena DO DO Santhush Weerakoon DO Email–firstnamelastname@hsbc.com.lk ABC Sri Lanka Markets Update USD/LKR Spot-closing (27 Jan 2015)=133.15/40 Inter-Bank call money ( 27 Jan 2015) 5.82% USD/LKR forward Premiums Treasury Bill Rates – Auction rates - net of tax SLIBOR 3 mth 145/175 cents 6 mth 280/320 cents 12 mth 520/580 cents 3 mth 6 mth 12 mth USD Sovereign Bond 2015 2020 O/Night 1 Month 3 Month 6 Month 12 Month 5.80% (5.79%) 5.90% (5.91%) 6.05% (6.04%) 3.04% 4.62% 5.91% 6.35% 6.57% 6.81% 7.11% Economic Indicators All share Price index S&P SL 20 Index Daily Turnover 7,367.65 up by 51.57 points (+0.70%) 4,130.43 up by 33.69 points (+0.82%) Rs. 1,128.56 million CBSL SDFR CBSL SLFR Statutory Reserve Ratio(SRR) 6.50% (January 2014) 8.00% (January 2014) 6.00% (June 2013) Consumers Price Index Inflation y-o-y % Inflation 12m moving ave 180.20 (Dec 2014) 1.6% (October 2014) 3.8% (October 2014) GDP Growth Gross Official Reserves Government Revenue Government Expenduture Unemployment 7.70% (2014 3Q) $ 7.37 Bn (Dec 2014) $ 8.75 Bn (2013 CBSL Annual Report) $ 12.84 Bn (2013 CBSL Annual Report) 4.5% (2014 2Q) Outstanding External debt $ 39.7 Bn (2013 CBSL Annual Report) Exports $ 898.50 mn (Oct 2014) Imports $ 1750.20 mn (Oct 2014) Trade Deficit $ -851.70 mn (Oct 2014) Derivatives – IRS (Bid) USD 0.7370 1.4660 1.9250 2 Year 5 Year 10 Year Central Bank rates NZD 3.50% GBP 0.50% CAD 0.75% CHF -0.75% GBP 0.8670 1.2621 1.5827 AUD USD EUR JPY AUD 2.4175 2.6100 2.9020 EUR 0.1088 0.2988 0.7238 2.50% 0.25% 0.05% 0.00% Stock Markets International Currency Markets DJI (USA) Nikkei 225 FTSE 100 17,813.98 (1.48%) 17,511.75 (1.05%) 6,796.63 (1.02%) USD/JPY GBP/USD EUR/USD AUD/USD USD/CAD Commodity Markets LIBOR - USD Gold IPE brent WTI 3 mth 6 mth 12mth $ 1,289.83 $ 49.06 $ 46.79 118.12 1.5162 1.1337 0.7990 1.2429 JPY/LKR GBP/LKR EUR/LKR AUD/LKR CAD/LKR 1.1268 201.80 150.89 106.35 107.08 0.2526% 0.3554% 0.6224% US Treasuries Asian Currencies 5 yr 10yr 1.4660% 1.9250% USD/IDR USD/INR 12,505 61.44 30yr 2.3050% USD/THB 32.63 Source: Reuters/Daily FT *All rates above are for indicative purposes only. 2 PUBLIC Sri Lanka Markets Update ABC FX Edge Asian FX: SGD: MAS lowers SGD NEER policy slope The MAS announced an unscheduled change of policy today, stating that the slope of the policy band within which the SGD NEER is managed “will be reduced, with no change to its width or the level at which it is centred”. This is the first unscheduled MPS since October 2001. The MAS was far more aggressive in its policy easing than we had expected and the market was clearly surprised by today’s announcement, with the SGD NEER falling initially by around 1.1% according to our model. Our estimate of the NEER is now trading around 0.7% above the bottom of the band (compared to 1.5% above bottom-bound pre-MPS). We believe the SGD NEER will fall to the lower bound of the band before the April MPS, as the market will speculate that this is not a one-off easing decision, but the start of an easing cycle. There is a risk that the MAS could ease further in April, by flattening the slope again (to a 0% slope), via a re-centring of the band lower, or by widening the band. We estimate that the new slope could be 0.5%, from 2.0% previously. This decision today means the MAS wants to open up room for outright depreciation in the SGD NEER in 2015. A 0.5% slope implemented today, assuming no other changes in band parameters in the rest of year means the SGD NEER can depreciate 1.3% from where it was trading at end-2014. Had MAS left policy unchanged in 2015, the SGD NEER can only at best manage zero percent appreciation. We recently revised our USD-SGD forecast to 1.40 by end-2015 (see Asian FX Focus: SGD: NEER a tipping point, 26 January 2015: https://www.research.hsbc.com/R/20/j3RNGH8). We are currently short SGD-IDR 3m NDF. We believe the urgency and the magnitude of the decision today reflects more than just concern about the domestic inflation outlook owing to lower oil prices. We believe the MAS appears concerned than it let on about the global economy, disinflationary forces and SGD over-valuation. The last policy easing took place in October 2011, amid the European debt crisis. This time, the MAS could be reacting to aggressive QE programs and negative interest rate policies taken by central banks in the G10 recently. One key difference between these periods lies in Singapore's weaker economic fundamentals today - the core inflation outlook is weaker, growth has been softer and productivity growth dismal leading to an over-valued SGD. As such, we believe the new slope setting is likely to be lower than the slope MAS shifted to in October 2011. We estimate that the new slope could be 0.5%, reduced by more than 1ppt because the MAS omitted the word “slightly” when talking about the slope reduction. We can verify this new assumption in April when MAS next provides an indication of where the SGD NEER has been trading within the policy band. There is a possibility the slope is only reduced to 1%. 3 PUBLIC Sri Lanka Markets Update This document is issued by The Hongkong and Shanghai Banking Corporation Limited (HSBC). The information contained herein is derived from sources we believe to be reliable, but which we have not independently verified. HSBC makes no representation or warranty (express or implied) of any nature nor is any responsibility of any kind accepted with respect to the completeness or accuracy of any information, projection, representation or warranty (expressed or implied) in, or omission from, this document. No liability is accepted whatsoever for any direct, indirect or consequential loss arising from the use of this document. Any examples given are for the purposes of illustration only. The opinions, if any, in this document constitute our present judgement, which is subject to change without notice. This document does not constitute an offer or solicitation for, or advice that you should enter into, the purchase or sale of any security, commodity or other investment product or investment agreement, or any other contract, agreement or structure whatsoever and is intended for institutional customers and is not intended for the use of private customers. The document is intended to be distributed in its entirety. This document is not a research report or a document for giving of investment advice. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. Unless governing law permits otherwise, you must contact a HSBC Group member in your home jurisdiction if you wish to use HSBC Group services in effecting a transaction in any investment mentioned in this document. This document, which is not for public circulation, must not be copied, transferred or the content disclosed, to any third party and is not intended for use by any person other than the intended recipient or the intended recipient's professional advisers for the purposes of advising the intended recipient hereon. Copyright. The Hongkong and Shanghai Banking Corporation Limited 2011. ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation 4 Limited. ABC The Hongkong and Shanghai Banking Corporation Limited Address:No 24 Sir Baron Jayatilake Mawatha, Colombo 1 Tel: +94 112 421697 Fax:+94 114 793575 Website: www.hsbcnet.com Website: www.research.hsbc.com PUBLIC

© Copyright 2025