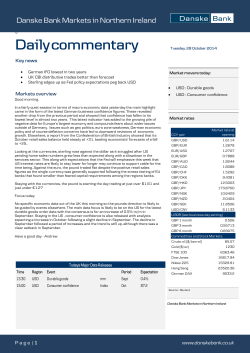

Weekly Credit Update

Weekly Credit Update 13 January 2015 Analyst Brian Børsting +45 45 12 85 19 brbr@danskebank.com Analyst Mads Rosendal +46 8 568 80594 madro@danskebank.com Important disclosures and certifications are contained from page 20 of this report. Contents - Market news - Trade ideas - Company news - Chart pack - List of official and shadow ratings and recommendations 2 What’s on our mind - General credit market news • After a relatively quiet start to the year in both the secondary and primary markets the new issue market has started to gain traction lately and the overall favourable market conditions could spur the primary market in the coming weeks. • Overall the credit market has started 2015 on a constructive note and activity could pick up further in the coming weeks. Sources: Bloomberg, Danske Bank Markets 3 Brian Børsting +45 45 12 85 19 brbr@danskebank.com BUY SASSS 2017 outright Attractive absolute value – supported by adequate liquidity Niklas Ripa +45 45 12 80 47 madro@danskebank.com • We believe SAS’ Q4 13/14 report was supportive from a credit perspective. This reflects the following. • • • • SAS has sufficient liquidity, in our view, to handle debt maturities to end-FY 2018. Cash and cash equivalents were SEK7.4bn at end-2013/14. Debt maturities to endFY 2018 are around SEK6.6bn. Cash flow from operations was solid, with SEK0.8bn in Q4 13/14 and SEK1.1bn for FY 2013/14. With limited capex for the coming years (SEK1bn expected in 2014/15) and financing secured for most aircraft deliveries in 2015-17, we expect SAS to be free cash flow positive in the years to come – and to be able to maintain adequate liquidity. We believe the SAS 2017 offers an attractive absolute return. SAS AB is rated B-/S with adequate liquidity. Due to the significant amount of pledged assets, we estimate the bond rating at CCC+/CCC. 900 800 SASSS 9 17 700 CCC B- 600 500 400 300 200 100 0 0 2 4 6 8 10 12 Years to maturity Debt maturity profile, SEKm 2500 2000 1500 1000 500 0 2021 2020 2019 2018 2017 2016 2015 SAS has hedged 43% of fuel consumption for the next 12 months. The positive impact is offset by a weaker SEK versus the USD but we estimate a positive net impact of SEK1-1.3bn for 2014/15. We expect the cost relief to support the bond valuation. Indicative SEK-equivalent ASW spread 1000 Note: As of 31 October 2014.; SAS’s financial year runs from November to October; hence, SAS AB 2017 bond expires in SAS’s financial year 2018; SAS AB 17 is a callable bond with first call 26 August 2016 @102.25, curve swapped to SEK Source: Bloomberg, SAS AB, Danske Bank Markets (both charts) 4 SELL ATCOA2019 2.625% – BUY ATCOA2023 2.500% The Atlas Copco 2019’s trade too tight for the rating, in our view • The Atlas Copco 2019s trade tighter than the average ‘A+’ rated EUR corporate. We suggest going further out on the curve and buying the Atlas Copco 2023s to get more value out of a fairly tight name. Alternatively, investors can sell 5YR protection on Atlas Copco for an even greater pick-up relative to the cash curve. • Atlas Copco has best-in-class low operational leverage as witnessed by its very strong margin protection in 2009. • Atlas Copco is exposed to Oil & Gas E&P capex spending. However, since its exposure is fairly well distributed over the entire Oil & Gas E&P value chain, downside to new orders in 2015 as a result of the lower oil price should be fairly limited, in our view. • • Having added substantial amounts of debt to its balance sheet with the acquisition of Edwards group in 2014, we view the risk of large scale M&A as limited in Atlas Copco. Our base case is that Atlas Copco continues with smaller bolt-on acquisitions in the first half of 2015. Key risk for the case is, in our view, a further decline in demand from the Mining segment in 2015. Mads Rosendal +46 8 568 80594 madro@danskebank.com Indicative ASW offer (bps) 60 EUR bonds - Investment Grade Industrials: BBB+ 50 40 Brian Børsting +45 45128503 brbr@danskebank.com ATCOA CDS EUR SR 5Y Industrials: A+ Industrials: A ATCOA '23 (A/A2) 30 20 10 0 2014 ATCOA '19 (A/A2) 2015 2016 2017 2018 2019 2020 2021 2022 2023 -10 Indicative YTM offer (%) EUR bonds - Investment Grade 1,0 Euro Swap yield curve A+/A/A- ATCOA '23 (A/A2) 0,5 ATCOA '19 (A/A2) 0,0 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 Benchmarked against a sample of highly liquid EUR corporate issues (min size: EUR500m, TTM: 1yr-10yrs) Source: Bloomberg (<SRCH>GO), Danske Bank Markets 5 Recent trade ideas Type Outright Trade SASSS '17 Curve spread Switch from ATCOA '19 to ATCOA '23 Idea We believe the SAS 2017 offers an attractive absolute value – supported by adequate liquidity Opened Start spread Outright Outright VLVY' 17 or VLVY'19 NYNAAB '18 The Atlas Copco 2019s trades tighter than the average ‘A+’ rated EUR corporate. Go out the curve and buy the '23s We see the VLVY cash curve as attractively valued and an (uncertain) downgrade is more than priced in to spreads NYNAAB '18's, which we see as 'B+' indicatively trade way too cheap relative to the industrial 'B+' curve Opened Start spread Opened Start spread Opened Start spread SAABAB '19 COMHSS '19 looks cheap compared to other rated and unrated issues in SEK. Trades like a B+, but is officially rated BBSKF’s 2020s and 2018s offer attractive value relative to the rating (‘BBB+’ NO and ‘Baa1’ S) Downgrade seems priced in already Trading wider than the ‘BBB+’ shadow rating would imply Swith from STENA '19 to STENA '20 Stena 2020 cheap compared with overall Stena credit curve and the Stena 2019 bond. Outright COMHSS '19 Curve spread Switch from SKFBSS '19 to SKFBSS '18 or '20 Outright Opened Start spread Opened Start spread Opened Start spread Curve spread Opened Start spread 18 dec 2014 807 18 dec 2014 16 27 nov 2014 72 25 nov 2014 640 19 nov 2014 450 18 nov 2014 2 13 nov 2014 115 24 okt 2014 126 See the end of this presentation for a list of our coverage including shadow ratings and recommendations Source: Danske Bank Markets 6 Company news from the past week Name SAS Carlsberg DFDS News SAS has released traffic figures for December 2014. Passenger traffic increased 0.2% y/y and due to slight capacity cutbacks utiliisation increased 1.2 p.p. y/y. More importantly currency adjusted average ticket prices increased by 1.5% y/y - this is positive in our view as SAS seems to be able to keep prices stable despite the declining oil price (largest cost item). This combination should - if this is a trend - translate into solid positive earnings in 2015. Although it is still early days for 2015 but we see the traffic figures as credit positive for SAS. We keep our Buy recommendation on the SAS 2017 bond. Late Friday Moody's affirmed the Baa2 rating on Carlsberg but changed the outlook to Negative from Stable. The Negative outlook reflects the ongoing deterioration in the Russian operating environment and prolonged weakness in the Euro to Ruble exchange rate. Due tothis Moody's expects it will be more challenging to maintain credit metrics in line with the Baa2 rating. In our view the Negative outlook is not a huge surprise due to the Russian debacle. We believe the negative impact from the deterioration in Russia will become more visible on 18 February where Carlsberg reports Q4 14 numbers and - not least - gives guidance for 2015. Should the current 12 months forward EUR/RUB rate hold for the rest of 2015 Carlsbergs EBIT could get hit by approximately DKK3bn compared to 2014. - which could affect Carlsbergs credit rating negatively. It should be noted that Carlsberg has stated commitment to Investment Grade status. We see the Carlsberg 5Y CDS as fairly priced and continue to see Carlsberg bond prices as unattractive - hence we keep our Sell recommendation. The Competition Appeal Tribunal last week decided to prohibit MyFerryLink (MFL) operating on the route between Dover and Calais (following a three year legal competition battle). MFL is owned by Eurotunnel and is one of DFDS´ competitors on the route. According to the ruling Eurotunnel will be forced to withdraw from this ferry activity and has therefore ordered ferry operations to cease within six months. We expect that the MFL volume is to be split equally between the three remaining operators (Eurotunnel ‘the tunnel’, DFDS and P&O-ferries) following the planned closure of MFL with an estimated positive annual effect in the area of some DKK100-150m pre-tax. Needless to say we regard the implications of this ruling positive for DFDS since the events to follow will likely increase future cash flows. We highlight that we continue to view DFDS’ credit profile as commensurate with a ‘BBB-’ indicative rating due to the healthy credit metrics and despite our expectation of increased future shareholder remuneration and the inherent moderate M&A event risk linked to the credit. The DKK DFDS 2019 bond currently trades some 10bps wider than the ‘BBB-‘ credit curve measured to CIBOR, not factoring in any discount for unrated nature of the issue, why we regard this bond as tightly priced for the time being. Investors able to hold NOK may consider switching from the DKK FRN 2019 bond into the NOK FRN 2016 or the NOK 2018 bond or buying any of these two NOK issues outright. These two NOK bonds seem to be priced with a discount to the ‘BBB-‘ curve measured to NIBOR of some 60bps and 30bps respectively giving a prospective investor some compensation for the limited liquidity and unrated nature of the issues - especially with regard to the NOK 2016 issue. Source: Danske Bank Markets Implication Credit positive Credit negative Credit positive 7 Selected new issues • The new issue market has started to gain traction. Selected new issues Date Issuer 07-01-2015 Abbey Natl Treasury Serv 07-01-2015 Rabobank Nederland 08-01-2015 Bnp Paribas 08-01-2015 Lloyds Bank Plc 08-01-2015 Volkswagen Intl Fin Nv 08-01-2015 Volkswagen Intl Fin Nv 08-01-2015 Volkswagen Intl Fin Nv Coupon 1,125% EUR003M +19bps EUR003M +40bps 1,25% EUR003M +30bps 0,875% 1,625% CCY EUR EUR EUR EUR EUR EUR EUR Volume 1 500 m 2 500 m 750 m 1 000 m 1 000 m 1 000 m 1 000 m Maturity Jan-22 Jan-17 Jan-20 Jan-25 Jul-18 Jan-23 Jan-30 S&P / Mdy / Fitch ASW/DM / A2e / Ae 65 / Aa2e / AA-e 19 / A1e / A+e 40 / / 55 / A3e / 30 / A3e / 40 / A3e / 65 Source: Danske Bank Markets 8 Chart pack: euro spreads and returns Euro IG ASW, iBoxx indices IG Total Return, iBoxx indices, 2014-01=100 Euro HY ASW, Merrill Lynch indices HY Total Return, Merrill Lynch indices, 2014-01=100 Source: Macrobond Financial, Danske Bank Markets [all charts] 9 Chart pack: relative value iTraxx vs iBoxx Nordic fin and non-fin corporates (IG) vs iTraxx Euro vs US CDS indices - IG (Markit) Euro vs US HY bond indices (Merrill Lynch) Source: Bloomberg, Macrobond Financial, Danske Bank Markets [all charts] 10 Chart pack: general market development European swap and government yields 3m TED-spread, US & Euro Area Euro swap curve spread Euro/USD basis swaps Source: Macrobond Financial, Danske Bank Markets [all charts] 11 Chart pack: fund flows Europe, net sales US, net sales Sweden, net sales Norway, net sales Source: Macrobond Financial, Danske Bank Markets [all charts] 12 Chart pack: macro GDP y/y growth, calendar adjusted Purchasing manager’s indices Euro area y/y chg in bank lending Euro area lending standards Source: Macrobond Financial, Danske Bank Markets [all charts] 13 Our coverage and shadow ratings 1 of 5 Company Ahlstrom Oyj Akelius Residential Ab Ambu A/S Ap Moeller - Maersk A/S Arla Foods Amba Atlas Copco Ab Avinor As Bank 1 Oslo Akershus As Bank Norwegian As Beerenberg Holdco Ii As Bw Offshore Cargotec Oyj Carlsberg Breweries A/S Cermaq Asa Citycon Oyj Color Group As Com Hem Holding Ab Danfoss A/S Danske Bank A/S Dfds A/S Dlg Finance As Dna Ltd Dnb Bank Asa Dong Energy A/S Dsv A/S Eg Holding Eika Boligkreditt As Eika Gruppen As Electrolux Ab Elenia Oy Elisa Oyj Entra Eiendom As Rating B+ BB+ BBBBBB+ Danske Bank Outlook Sr. Unsec Stable Pos BB Stable Stable Stable Stable Stable Stable BB Stable BB- Stable BBB B ABBB A- Moody's Rating Outlook BBB+ Stable Baa1 Stable A AA- Stable Stable A2 A1 Stable Stable Baa2 Stable Fitch Rating Outlook Stable BBB+ BBB B+ BB+ BBB- BBBBBBBB- S&P Rating Outlook BBB Stable Baa2 Stable BBBBB A Stable Stable Neg A3 Stable BBB Stable A Stable B+ Stable Stable Stable A+ BBB+ Stable Stable A1 Baa1 BBB Stable Wr BBB Pos Baa2 Neg Stable BBB+ Stable Stable Stable Stable Stable WD Stable Stable Analyst(s) Mads Rosendal Louis Landeman Jakob Magnussen Brian Børsting Mads Rosendal Mads Rosendal Ola Heldal T. Hovard / L. Holm T. Hovard / L. Holm Øyvind Mossige Øyvind Mossige Mads Rosendal Brian Børsting Knut-Ivar Bakken Louis Landeman Niklas Ripa Ola Heldal Jakob Magnussen Niklas Ripa Mads Rosendal Ola Heldal T. Hovard / L. Holm Jakob Magnussen Brian Børsting Jakob Magnussen T. Hovard / L. Holm T. Hovard / L. Holm Brian Børsting Jakob Magnussen Ola Heldal Ola Heldal Recomm. BUY SELL HOLD SELL HOLD HOLD HOLD BUY BUY 14 Our coverage and shadow ratings 2 of 5 Danske Bank Company Rating Outlook Sr. Unsec Farstad Shipping Asa BB Neg BBFingrid Oyj Finnair Oyj BB Stable Fortum Oyj Fortum Varme Holding Samagt Med Stockholms Stad Ab Fred Olsen Energy Asa BB+ Neg G4S Plc Getinge Ab BB+ Neg Golden Close Maritime Corp Ltd B Heimstaden Ab BB Stable BBHemso Fastighets Ab BBB+ Stable BBB Hkscan Oyj BB Stable Hoist Kredit Ab BBStable B+ Husqvarna Ab BBBPos Ikano Bank Ab BBB Stable Investor Ab Iss A/S J Lauritzen A/S B Stable BJernhusen Ab AStable Jyske Bank A/S Kesko Oyj BBB Stable Klaveness Ship Holding As BBStable B+ Loomis Ab BBBStable Luossavaara-Kiirunavaara Ab BBB+ Stable Meda Ab BBStable Metsa Board Oyj Metso Oyj Ncc Ab BBBStable Neste Oil Oyj BBBStable Nokia Oyj Nokian Renkaat Oyj BBB+ Stable Nordea Bank Ab S&P Rating Outlook Moody's Rating Outlook Fitch Rating Outlook A+ Stable A1 Stable A+ Stable ABBB+ Neg Stable A2 Neg A- Neg BBB- Stable AABBB- Stable Stable A1 Stable A- Stable Baa1 Neg B+ BBB Pos Stable B1 Baa2 Pos Stable BB Pos Ba2 Pos BB Stable AA- Neg Aa3 Neg AA- Stable Analyst(s) Øyvind Mossige Jakob Magnussen Brian Børsting Jakob Magnussen Jakob Magnussen Sondre Stormyr Brian Børsting Louis Landeman Sondre Stormyr Louis Landeman Louis Landeman Brian Børsting Gabriel Bergin Louis Landeman T. Hovard / L. Holm Brian Børsting Brian Børsting Bjørn Kristian Røed Gabriel Bergin Thomas M. Hovard Mads Rosendal Bjørn Kristian Røed Brian Børsting Louis Landeman Louis Landeman Mads Rosendal Mads Rosendal Louis Landeman Jakob Magnussen Ola Heldal Jakob Magnussen T. Hovard / L. Holm Recomm. BUY SELL BUY BUY HOLD BUY HOLD HOLD HOLD SELL 15 Our coverage and shadow ratings 3 of 5 Company Norwegian Air Shuttle Asa Norwegian Property Asa Nykredit Bank A/S Nynas Group Odfjell Se Olav Thon Eiendomsselskap Asa Olympic Shipping As Orkla Asa Outokumpu Oyj Pohjola Bank Oyj Posten Norge As Postnord Ab Prosafe Se Ramirent Oyj Saab Ab Sampo Oyj Sandnes Sparebank Sandvik Ab Sas Ab Sbab Bank Ab Scania Ab Schibsted Asa Seadrill Ltd Securitas Ab Skandinaviska Enskilda Banken Ab Skanska Ab Skf Ab Sognekraft As Solstad Offshore Asa Spar Nord Bank A/S Sparebank 1 Boligkreditt As Sparebank 1 Nord Norge Rating BBBBB- Danske Bank Outlook Sr. Unsec Stable B+ Stable B+ B+ BBB+ B+ BBB+ B Stable Stable Stable Stable Pos Pos ABBB+ BB BB+ BBB+ Stable Stable Stable Stable Stable BBB+ Stable BBB BB+ Stable Stable BBB+ Stable BBB BBBBB+ A- Stable Stable Stable Stable S&P Rating Outlook Moody's Rating Outlook Fitch Rating Outlook A+ Neg Baa2U Stable A Stable AA- Neg Aa3 Neg A+ Stable Wr Baa2 Stable B+ B B BBB BA A- Neg Stable Neg Stable Wr A2 Stable Neg BBB A+ Stable Neg Wr A1 Neg BBB+ Neg Baa1 Stable A2 Neg BB A+ Pos BBB B+ A Stable Analyst(s) Brian Børsting Ola Heldal T. Hovard / L. Holm Jakob Magnussen Bjørn Kristian Røed Ola Heldal Øyvind Mossige Ola Heldal Mads Rosendal T. Hovard / L. Holm Ola Heldal Gabriel Bergin Sondre Stormyr Brian Børsting Louis Landeman T. Hovard / L. Holm T. Hovard / L. Holm Mads Rosendal Brian Børsting T. Hovard / L. Holm Mads Rosendal Ola Heldal Sondre Stormyr Brian Børsting T. Hovard / L. Holm Louis Landeman Mads Rosendal Jakob Magnussen Øyvind Mossige T. Hovard / L. Holm Lars Holm T. Hovard / L. Holm Recomm. HOLD SELL HOLD HOLD HOLD HOLD HOLD BUY SELL HOLD 16 Our coverage and shadow ratings 4 of 5 Company Sparebank 1 Smn Sparebank 1 Sr-Bank Asa Sponda Oyj St1 Nordic Oy Statkraft Sf Statnett Sf Statoil Asa Steen & Strom As Stena Ab Stockmann Oyj Abp Stolt-Nielsen Ltd Stora Enso Oyj Storebrand Bank Asa Suomen Hypoteekkiyhdistys Swedavia Ab Swedbank Ab Swedish Match Ab Svensk Fastighetsfinansiering Ab Svenska Cellulosa Ab Sca Svenska Handelsbanken Ab Sydbank A/S Tallink Group As Tdc A/S Teekay Offshore Partners Lp Tele2 Ab Telefonaktiebolaget Lm Ericsson Telenor Asa Teliasonera Ab Teollisuuden Voima Oyj Thon Holding As Tine Sa Upm-Kymmene Oyj Rating BBBBB Danske Bank Outlook Sr. Unsec Stable B+ BB+ Stable Stable BBB+ AA- Stable Stable Stable Fitch Rating Outlook AStable AStable AA+ AA- Stable Stable Stable Aaa Wr Aa2 Stable Stable Stable BB Stable B2 Stable BB BBB+ Stable Neg Ba2 Baa2 Stable Neg WD A+ BBB Neg Stable A1 Baa2 Neg Stable A+ Pos AAA- Stable Neg Baa1 Aa3 Baa1 Stable Neg Neg AA- Stable BBB Neg Baa3 Stable BBB Stable BBB+ A ABBB Stable Stable Stable Neg Baa1 A3 A3 Wr Stable Stable Neg BBB+ Stable ABBB Stable Stable BB+ Stable Ba1 Stable WD BB Stable BB Stable BB- BBBBB Stable Stable B+ BBB+ BBB+ Moody's Rating Outlook A2 Neg A2 Neg Stable Stable BBB+ BBB S&P Rating Outlook Stable Stable Analyst(s) Recomm. T. Hovard / L. Holm T. Hovard / L. Holm Louis Landeman Jakob Magnussen Jakob Magnussen Jakob Magnussen Jakob Magnussen Ola Heldal Niklas Ripa Mads Rosendal Bjørn Kristian Røed Mads Rosendal T. Hovard / L. Holm T. Hovard / L. Holm Gabriel Bergin T. Hovard / L. Holm Brian Børsting Louis Landeman Mads Rosendal T. Hovard / L. Holm T. Hovard / L. Holm Niklas Ripa Ola Heldal Bjørn Kristian Røed Ola Heldal Ola Heldal Ola Heldal Ola Heldal Jakob Magnussen Ola Heldal Ola Heldal Mads Rosendal HOLD HOLD BUY HOLD SELL BUY HOLD BUY HOLD BUY HOLD BUY HOLD HOLD HOLD SELL BUY HOLD 17 Our coverage and shadow ratings 5 of 5 Company Vasakronan Ab Vattenfall Ab Vestas Wind Systems A/S Victoria Park Ab Wilh Wilhelmsen Asa Volvo Ab Rating ABBBBBBBB- Danske Bank Outlook Sr. Unsec Stable Pos Stable Stable S&P Rating Outlook Moody's Rating Outlook Fitch Rating Outlook A- Stable A3 Stable A- Neg BBB Neg Baa2 Neg BBB Stable B+ Analyst(s) Louis Landeman Jakob Magnussen Niklas Ripa Louis Landeman Bjørn Kristian Røed Mads Rosendal Recomm. HOLD BUY BUY Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets 18 Fixed Income Credit Research team Thomas Hovard, Chief Analyst Head of Credit Research +45 45 12 85 05 hova@danskebank.com Brian Børsting, Senior Analyst Industrials +45 45 12 85 19 brbr@danskebank.com Ola Heldal, Analyst TMT +47 85 40 84 33 olh@danskebank.com Louis Landeman, Analyst TMT, Industrials +46 8 568 80524 llan@danskebank.com Lars Holm, Senior Analyst Financials +45 45 12 80 41 laho@danskebank.dk Sondre Dale Stormyr, Analyst Offshore Rigs +47 85 40 70 70 sost@danskebank.com Mads Rosendal, Analyst Industrials, Pulp & Paper +46 8 568 80594 madro@danskebank.com Gabriel Bergin, Analyst Strategy, Industrials +46 8 568 80602 gabe@danskebank.com Henrik René Andresen, Analyst Credit Portfolios +45 45 13 33 27 hena@danskebank.com Jakob Magnussen, Senior Analyst Utilities, Energy +45 45 12 85 03 jakja@danskebank.com Niklas Ripa, Senior Analyst High Yield, Industrials +45 45 12 80 47 niri@danskebank.com Øyvind Mossige, Senior Analyst Oil Services +47 85 40 54 91 omss@danskebank.com Knut-Ivar Bakken, Analyst Fish Farming +47 85 40 70 74 knb@danskebank.com Bjørn Kristian Røed, Analyst Shipping +47 85 40 70 72 bred@danskebank.com 19 Disclosures This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske Bank’). Analyst certification Each research analyst responsible for the content of this research report certifies that the views expressed in the research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report. Regulation Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request. The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’ rules of ethics and the recommendations of the Danish Securities Dealers Association. Conflicts of interest Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank. Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions. Danske Bank, its affiliates and subsidiaries are engaged in commercial banking, securities underwriting, dealing, trading, brokerage, investment management, investment banking, custody and other financial services activities, may be a lender to the companies mentioned in this publication and have whatever rights are available to a creditor under applicable law and the applicable loan and credit agreements. At any time, Danske Bank, its affiliates and subsidiaries may have credit or other information regarding the companies mentioned in this publication that is not available to or may not be used by the personnel responsible for the preparation of this report, which might affect the analysis and opinions expressed in this research report. See http://www-2.danskebank.com/Link/researchdisclaimer for further disclosures and information. 20 General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’). The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report. The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report. This research report is not intended for retail customers in the United Kingdom or the United States. This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written consent. Disclaimer related to distribution in the United States This research report is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for distribution in the United States solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to ‘U.S. institutional investors’. Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction. Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of nonU.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission. 21

© Copyright 2025